Skip to content

book your free

consultation

02037355119

Resources

How We Work

For StartUp

For General Business

Case Study

Loopr LTD

Darran Smith

Sunstone IP Systems Ltd

Pricing

About Us

Services

Career

Contact Us

Menu

Resources

How We Work

For StartUp

For General Business

Case Study

Loopr LTD

Darran Smith

Sunstone IP Systems Ltd

Pricing

About Us

Services

Career

Contact Us

Linkedin-in

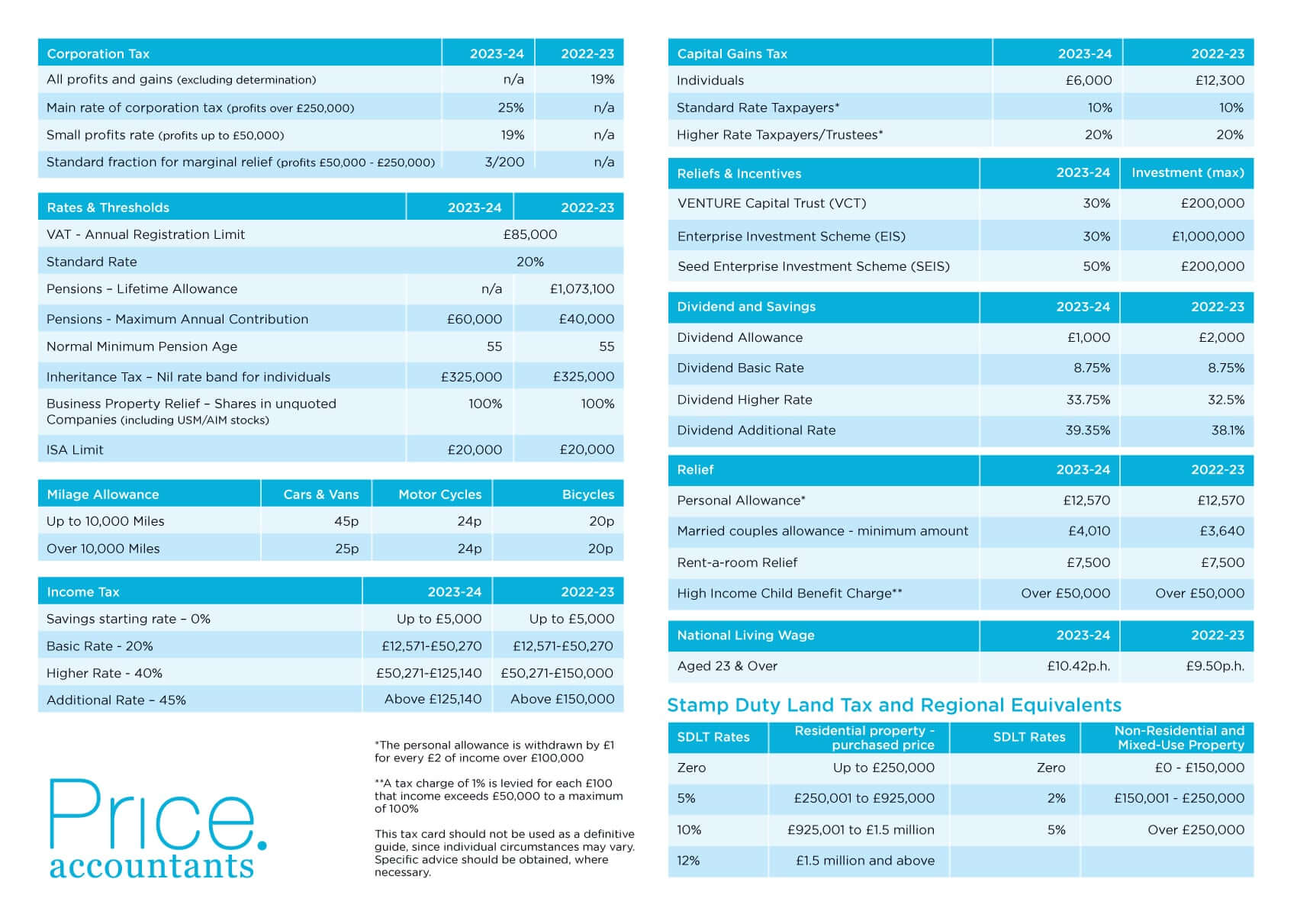

Download our tax card

Download full tax card

Let’s work together!

Contact us

Book a meeting

Download full tax card

Name *

Phone number *

E-mail *

Company name

Download

Resources

How We Work

For StartUp

For General Business

Case Study

Loopr LTD

Darran Smith

Sunstone IP Systems Ltd

Pricing

About Us

Services

Career

Contact Us

Resources

How We Work

For StartUp

For General Business

Case Study

Loopr LTD

Darran Smith

Sunstone IP Systems Ltd

Pricing

About Us

Services

Career

Contact Us

Linkedin-in

book your free consultation

02037355119